While the last 5 years of super easy Fed policy has not generated the economic growth or jobs as hoped for, stock prices have soared and lending standards are beginning to wane. It appears that stock prices are being driven more by valuation expansion than revenue growth, which is unsustainable, and could be indicative of a bubble. Easy policy has incentivized a rotation out of lower yielding securities to fund speculation in higher yielding assets and securities like stocks. There are also indications that commercial and industrial (C&I) loan lending standards are falling as banks desperately struggle for business, which could also be a sign of an impending bubble.

These indications seem all too familiar in an environment with a highly accommodative Fed. The question is can the Fed reverse its most accommodative policy in history fast enough to prevent another bubble and subsequent bust? The anticipated Fed plan of reducing Quantitative Easing (QE) purchases at $10 billion increments over the next 7 meetings would not end the purchase program until the December 16-17th, 2014 meeting. At this pace by the time QE is phased out, and the zero interest rate tether is released, it might too late to prevent a third bubble in only 20 years. The Fed has a history of not switching to tighter policy aggressively enough after years of overtly easy policy.

[Read More: Former Fed President Admits Central Banking, Paper Money a "Confidence Game"]

In 2002, after 2 years of tech bubble deleveraging, a deflation scare prompted the Federal Reserve to conduct aggressive monetary policy aimed at lowering the inter-bank (Fed Funds) lending rate from over 5% to 1%. The easy policy incentivized risky spread trading, as institutions and individuals borrowed cheaply to fund speculation of higher yielding stocks and real estate. In 2004 with asset prices steadily rising, the Fed switched gears and began to tighten policy in an attempt to rein in the rampant run up.

Despite the change to tighter Fed policy, by the summer of 2005 stock and real estate prices had surged to a level that evoked concern of a bubble. Contrary to that concern, in a July 2005 interview with the then Chairman of Economic Advisors Ben Bernanke, Maria Bartiromo of CNBC asked, “What is the worst-case scenario? We have so many economists coming on our air saying ‘oh, this is a bubble, and it’s going to burst, and this is going to be a real issue for the economy.’ Some say it could even cause a recession at some point. What is the worst-case scenario if in fact we were to see prices come down substantially across the country?” Bernanke responded, “Well, I guess I don’t buy your premise. It’s a pretty unlikely possibility. We’ve never had a decline in house prices on a nationwide basis. So, what I think is more likely is that house prices will slow, maybe stabilize, might slow consumption spending a bit. I don’t think it’s going to drive the economy too far from its full employment path, though.”

Bernanke’s unperturbed comments appeared grossly mis-guided less than 2 years later as a surge in subprime mortgage delinquencies led to sub-prime lender New Century filing for bankruptcy in April 2007. The Fed switched policy again and began implementing easy monetary policy in an effort to offset pending deflationary pressures. Shortly after the Fed began implementing lower interest rate policy, the over-levered U.S. economy awash with subprime mortgage debt finally collapsed as stocks and asset prices crashed.

[Don't Miss: Dr. Peter Warburton: Disinflationary Trend Continuing - But Fed's QE Policy Ultimately Leads to Higher Inflation]

Years of excessive credit had led to massive increases in stock and asset prices. The key being that the rise in prices was not fueled by increased productivity, it was fueled by increased availability of credit along with a social acceptance of using excess credit for gratuitous spending and speculation.

Figure 1 — The Fed Funds Target Inter-Bank Interest Rate

By December 2007, the economy officially entered a balance sheet recession awash with massive deleveraging. The population became less creditworthy and less confident in future income, and balance sheets contracted as loans were closed out and minimal new credit was issued.

By the end of 2008, the Fed had lowered the Fed Funds target rate to zero. The Fed hoped that driving down interest rates would make outstanding loans less expensive and new credit creation more attractive (see Figure 1), resulting in new money that could be used to stabilize crashing asset prices.

The Fed set out to achieve its target rate using open market operations, which is the Feds traditional method of manipulating interest rates. [Using open market operations, the Fed creates money out of thin air and uses the newly created money to buy Federal government bonds (ie. treasuries) via repos from the Feds Primary Dealers (see Figure 2). With this process, the Fed swaps treasuries on bank balance sheets with cash reserves, which lowers the inter-bank lending rate because a greater supply of reserves available reduces the “market price” of banks borrowing reserves from each other.]

Figure 2 — The Federal Reserve’s Primary Dealers as of February 2014

In addition to regular open market operations, in October 2008 the Fed entered a new territory of stimulus as it began paying banks interest on reserves held at the Fed for the first time in history. The Fed hoped that this interest income would help recapitalize banks, and would also give the Fed another tool to use when targeting the Fed Funds rate. The thinking being that banks would not lend out reserves for less than what the Fed is paying them, in this case 0.25%. Paying banks interest on reserves held at the Fed was an important development of the current stimulus program given that the Fed’s open market operations, and later QE, were effectively based on building up bank reserves held at the Fed.

When the Feds target zero interest rate level was realized in December 2008, deleveraging of the economy was still accelerating and asset and stock prices were far from normalized. The Fed had a mission to continue with stimulus, but having already taken rates to the floor, the Fed chose to experiment with a more targeted asset purchase program referred to as Quantitative Easing.

[The mechanics of QE are similar to open market operations, in that the Fed again creates money out of thin air, but instead of using the money to buy treasuries, the Fed buys mortgage backed securities (MBS) and government bonds with longer maturities than treasuries. This process swaps toxic MBS with cash reserves, leaving private balance sheets cleaner. QE significantly benefits banks as the Fed not only takes these unwanted assets off of their balance sheets, but pays them a premium to do so, the difference essentially equating to a cash infusion. In addition, the Feds Primary Dealers (see Figure 2) also receive cash commissions from the Fed for these transactions.]

QE1 was the first time the Fed ever bought mortgage bonds, and it was the most aggressive stimulus program initiated in the Feds 100 year history, buying .55 trillion worth of assets in 12 months. Andrew Huszar, a Fed official that oversaw QE implementation described the execution as “buying so many (mortgage bonds) each day through active, unscripted trading that we constantly risked driving bond prices too high and crashing global confidence.”

By the time QE1 was complete, the cost of bank lending had decreased as planned, but it did not matter because banks were still not lending (see Figures 3-8). Creditworthiness and confidence, essential for credit creation, had still not returned to the U.S economy. Even though QE1 delivered lackluster results, the Fed proceeded with QE2 only 7 months after QE1 purchases were complete. QE2 was a continuation of QE1 targeting MBS and long bonds, buying 0 billion worth of securities over 6 months.

Figure 3 — C&I Loans by Large Banks, 2003-Present

Figure 4 — C&I Loans by Small Banks, 2003-Present

Figure 5 — Consumer Loans by Large Banks, 2003-Present

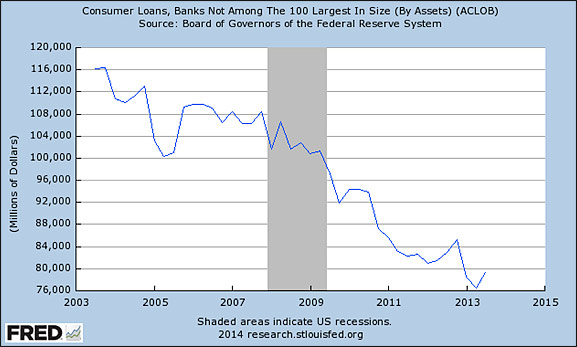

Figure 6 — Consumer Loans by Small Banks, 2003-Present

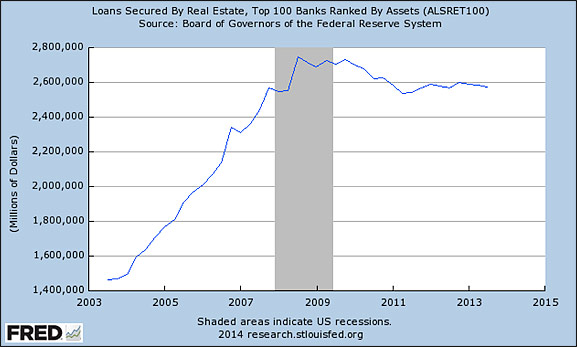

Figure 7 — Mortgage Loans by Large Banks, 2003-Present

Figure 8 — Mortgage Loans by Small Banks, 2003-Present

In September 2012, a third –this time open-ended– round of QE was announced. Originally billion a month of purchases was raised to billion only two months later, with the purchases specifically targeting mortgage backed securities.

As of February 2014 QE3 continues strong, although a so-called “tapper” has since reduced purchases to billion from billion a month.

It’s been over 5 years since the Fed began engaging in easy monetary policy. Over that time the Feds balance sheet has grown to a record + trillion from less than trillion (See Figure 9). More than half of the balance sheet expansion is now in the form of interest baring bank reserves held at the Fed, which stand at over .4 trillion (See Figure 10). By building up bank reserves, the Fed has essentially removed the burden of reserve requirements without actually removing the reserve requirements. With excess reserves, banks can create loans and make subsequent deposits without the need to borrow at the inter-bank rate to cover their reserve requirement. [A reserve requirement is the minimum amount of money that a bank must hold against its deposits, which adjusts as new credit is created and deposited.]

[Hear More: Ronald Stoeferle: Monetary Tectonics - The Tug of War Between Inflation and Deflation]

Figure 9 — Total Assets of Federal Reserve, 2004-Present

Figure 10 — Total Reserves Held At Federal Reserve, 2004-Present

Even after 5 years of the Feds most aggressive accommodative policy in history, there is still a lack of hoped for quality credit creation in the economy, which could be a sign that the greatest deleveraging of the U.S. economy since the Great Depression is still not complete. The Feds unrelenting dovish policy appears to support this concern.

Today, looking into specific trends in credit creation, what appears to be strong commercial and industrial loan growth (see Figures 3, 4) is primarily the result of lower lending standards as desperate banks compete for business by offering weaker covenant structures. Also, a large portion of C&I loans are being used to refinance existing loans and to pay for regular business maintenance, not new growth and expansion. Consumer lending by large banks (see Figure 5) has been non-existent ever since an initial spike back in late 2009, and consumer lending by small banks (see Figure 6) is still declining at the same pace as it was in the heart of the deleveraging period. Mortgage lending by large (see Figure 7) and small banks (see Figure 8) has still not shown any indication of growth over the last 5 years.

[Related: On Its 100th Birthday, the Fed Gives the World Another Stock Market Bubble]

While the Feds policy has arguably failed to create the kind of credit and confidence needed for real job growth and meaningful economic expansion, the policy has driven large-cap stock prices, measured by the S&P 500 to an all time high. However, it is important to note that stock valuations are rising at a faster pace than corporate revenues, meaning that a lot of the stock price appreciation has been the result of price/earnings multiples expanding, not revenue growth. Bottom-line corporate profits of S&P 500 components have improved from 2008/09 levels, but frequently at the expense of unsustainable cost cutting, which is counter-supportive of future growth. Nominal stock prices at this level can be misleading without proper analysis.

Very low interest rate environments have historically drawn money from bonds and into stocks. Potential stock returns appear appealing on a relative basis when compared to bonds with low single digit returns or less. An aggressive rotation into stocks has historically occurred in recent very low interest rate environments such as the tech bubble of the late 1990’s and in the most recent housing bubble. In both of these examples, stocks had run ups lasting approximately 5 years following highly accommodative Federal Reserve policy, before consequently crashing. The most recent stock market rally, having commenced in March 2009, is almost 5 years in the works (see Figure 11).

Figure 11 — S&P 500, 1994-Present

If history is a guide, as deleveraging completes, creditworthiness returns; confidence picks up; the last 10 years are forgotten (as is human nature); and excess borrowing fueled by too-easy Fed policy once again becomes the social norm. Current stock prices and C&I loan activity appear to be indicative of this pattern. The current Fed policy incentivizes cheap borrowing, resulting in risky spread trading, chasing already inflated stocks and other higher yielding assets. In the past the Fed has not been able to reverse policy fast enough to combat rising prices before over speculation ensues and borrowing and prices are pushed to unsustainable levels, and then bust. So far, this time around does not appear to be any different.