Louis Gave at Gavekal Research says the greatest source of potential instability in the years ahead lies with the massive growth of the U.S. corporate debt market, particularly at the BBB-rated (near junk) level.

Gave recently told FS Insider that it has far outpaced the economy and could be due for a reset during the next downturn, which is increasingly becoming a concern by other strategists.

When it comes to potential trouble spots brewing in the financial markets or global economy, Gave said “if you ask a French client, they tend to point a finger at Italy. If you ask Italian clients, they point a finger at Deutsche Bank; and if you ask German clients, they point a finger at France. When I talk to my U.S. clients, most of them point a finger at China, which they see as having unsustainable high levels of debt and is an accident waiting to happen.”

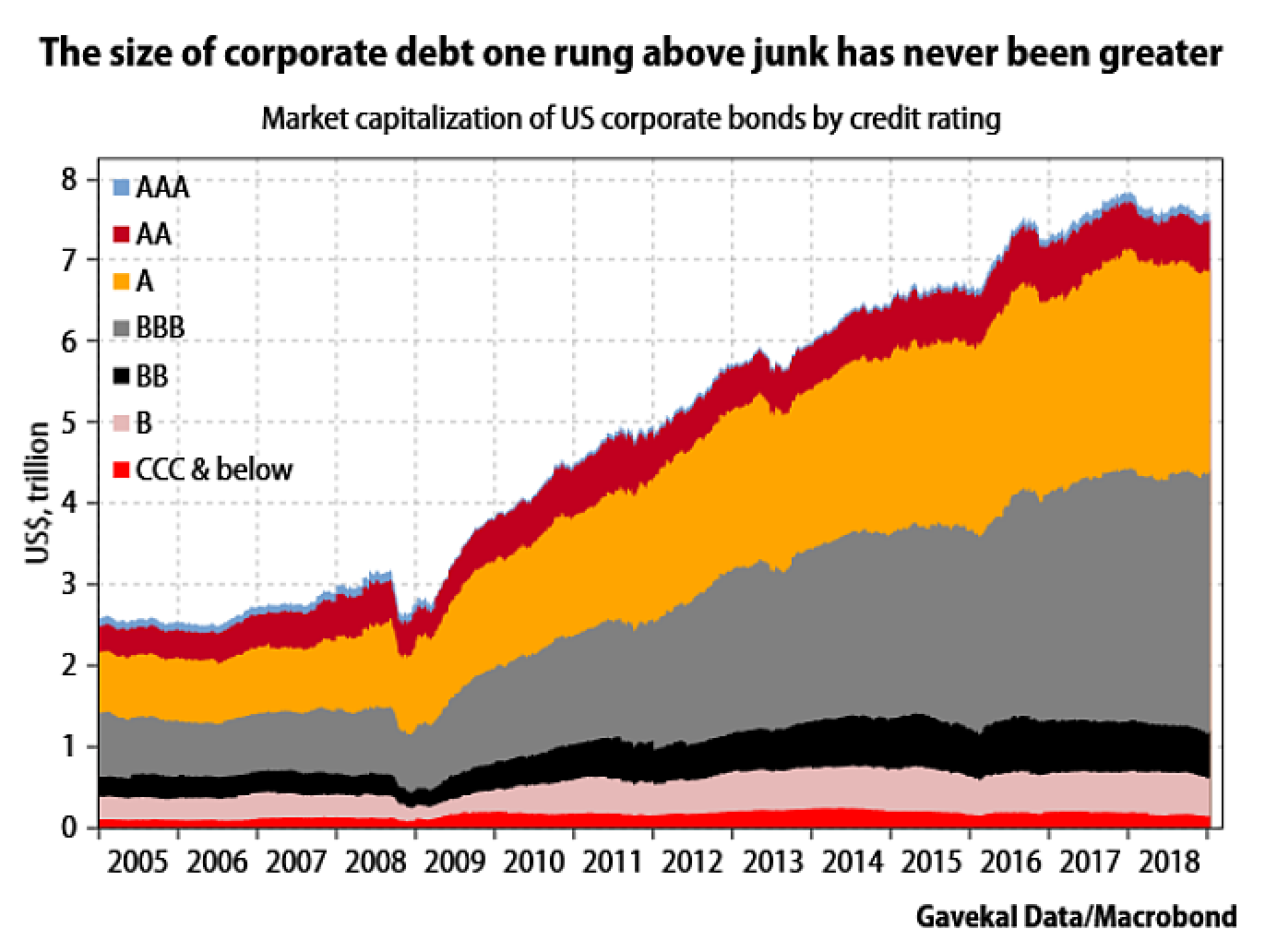

However, Gave sees an even source of potential problems since, as he points out, the "size of corporate debt one rung above junk has never been greater" (see below).

The challenge today, Gave said, “is that part of the massive growth we’ve seen in the U.S. corporate bond market has really taken place in the BBB space. And so, if you start seeing an economic downturn (and the usual type of downgrades that occur in a downturn), then all of a sudden you have investment grade that becomes non-investment grade.”

Gave worries this could send shock waves through the financial markets since U.S. corporate debt is widely held by pension funds, investment banks, and large institutions all around the globe.

“There are real questions about all the energy debt that’s being issued by a lot of negative cash flow companies in the energy space,” he said, which also leads to questions about industrial, auto and real estate debt.

Gave asked listeners whether all this growth in debt has "funded the purchase of assets that allow the servicing of the debt and then the reimbursement of the debt or has this growth really funded a massive rise in share buybacks and financial engineering?” Gave said if the answer is the latter it would signify that our balance sheets are far more stretched out than they have been in pervious cycles.

Listen to this full interview by clicking here. Not a subscriber? Click here.