“The farther backward you can look, the farther forward you are likely to see.”

-Winston Churchill

“There are two kinds of forecasters: those who don’t know, and those who don’t know they don’t know.”

-John Kenneth Galbraith

The word "oracle" stems from the Latin verb orare, meaning to pray or to speak. In the ancient world a priest or a priestess served as a portal in which the gods spoke directly to humans. Oracular shrines dotted the landscape in antiquity as they do today—only in different form. In the Old World, oracles were a branch of divination and were ubiquitous throughout the ancient world. Today we don’t call them oracles. They are known by other names: weatherman, forecaster, strategist, or the Fed Chairman.

Before the days of scientific knowledge, oracles were sought out for clarity in civil matters, issues of state, war or religion. We still seek their advice today in wanting to know where the economy is headed, where the stock market will end up by year-end or what the direction of interest rates will be. In our modern world, the most well-known oracle is Jerome Powell, chairman of the Federal Reserve. Instead of Delphi and Mount Olympus we have Federal Open Market Committee meetings and Wall Street.

Despite today’s rapid advancements in science and technology, the traditions of the oracle remain with us. Like the unknowns of the ancient world, today’s markets are made up of so many unknowns: How many times will the Fed raise interest rates this year? Where will the S&P 500 be by year-end? Will the economy grow, or will another recession take the place of growth? Will stocks, bonds, or cash be the better investment this year?

Trying to predict markets is a perilous task at the best of times, far more difficult in the final stages of a Fed rate-raising cycle. If you look at how forecasts are made on Wall Street, analysts start with an estimate of what they think S&P 500 earnings will be and then assign a PE multiple to those earnings estimates. The difference between forecasts generally reflects the bullish or bearish biases of the strategists or analysts making them.

Our own views do not reflect a specific number. They are more event driven. To quote numerous Fed governors and chairmen: “We are data dependent.” Our own theme for the year is Fast and Furious: Time to Buckle Up. The combination of numerous risks make our predictions less certain since specific events will ultimately lead to different outcomes.

We see three main risks for 2019:

- A Fed Policy mistake

- Escalation of the trade war between the U.S. and China

- Political discord: Democrats investigate instead of legislate

Two lesser risks:

- Oil spikes

- Cyber attacks on infrastructure

Before I delve into our own views of the economy and markets, I would like to begin with the consensus.

| 2019 | 2020 | |

| GDP | 2.6% | 1.9% |

| Inflation | 2.2% | 2.2% |

| Unemployment | 3.6% | 3.6% |

| Fed funds rate | 3.05% | 2.95% |

| 10-year yield | 3.29% | 3.37% |

When it comes to the stock market, Wall Street is bullish for 2019. Here are the forecasts for the S&P 500:

| High forecast | 3,250 |

| Low forecast | 2,665 |

| Average | 2,975 |

| Median | 2,980 |

Given the events of fourth quarter last year it is hard to find any bears on Wall Street for 2019. The projected forecasts for this year range from six to eight percent on the low end, 18-20 percent on average and over 30 percent on the high end. Wall Street is bullish. But as our friend Gary Shilling is fond of saying, they are paid to be bullish.

There is some talk of a probable recession either late this year or by 2020. If that is the case, it isn’t reflected in any of the Wall Street forecasts compiled by Bloomberg.

Our theme for this year is Fast and Furious: Time To Buckle Up

We expect volatility to be greater than last year and to be fast and furious when it happens. Think of February last year when record gains in January were given back in just six days. A different example is the price of oil which went from a bull market to a 40 percent decline in a bear market, only to rise over 25 percent in just a few weeks—all over the course of two months. We expect more of the same this year with lift and downdrafts to be more frequent and severe, depending on event outcomes.

I would like to overlay three other risks that could exasperate market volatility. These risks emerged out of the financial crisis and are trends that, when combined with our three macro risks, create an environment prone to flash crashes, fast and furious lifts and down drafts. I began to articulate these themes in early 2017. They are as follows:

- The passive index investing bubble

- Financial concentration

- Shrinking market liquidity

A number of these factors were at play last year both in the February stock market correction, the rise of the FAANG stocks and in the sudden crash in oil prices.

For more information on these three risk factors please see the links to my podcasts for more in-depth discussions on these topics below.

- Inside the Bubble (Passive index investing)

- Financial Concentration

- The Factor (Liquidity Risks)

Passive indexing, shrinking liquidity and financial concentration all played a role in 2018, exasperated by algorithmic, or "algo", trading. The markets have become much more difficult to anticipate over the last few years as new technologies evolved while traditional active managers and human judgment has been replaced by computerized models or machines.

High frequency trading (HFT) is wreaking havoc on markets and making old fashioned fundamental analysis and common sense obsolete. The combination of what happened last February, with the oil markets last fall and the stock markets in December, is only the beginning. We saw big draw downs in stocks despite very little fundamental economic news, making last December the worst December since the depression year of 1931.

In the words of one former hedge fund manager, Stanley Druckenmiller, “These algos have taken the rhythm out of the markets and have become confusing to me.”

According to the Financial Times and a study conducted by JP Morgan, only about 10 percent of U.S. equity trading is now done by traditional investors. The first clue that markets had changed was the 2010 Flash Crash where in just 36 minutes the S&P 500 crashed eight percent and then rebounded back to where it started. February of last year was another example of what I am calling fast and furious, the new market norm. Corrections or bear markets don’t happen over several years, months or weeks. They can happen in minutes, a day or a week. Think of a falling elevator, not an escalator on the way down.

The markets and the way they function have changed dramatically. Quantitative analysts, or "Quants", and HFTs now account for over half of all U.S. equity trading. Throw in index funds and we have mindless investing that at times can turn on a dime and become divorced from fundamentals, making these markets much more difficult to navigate.

What makes this more hazardous are these players can all intersect at the same time during periods of market stress. The problem with HFT-dominated markets is that they have far less capital than major banks, so when things get bumpy or mayhem breaks out in trading, they can withdraw liquidity, rapidly removing a floor underneath the markets. They have no choice given their thin capitalization. They withdraw from battle, lick their wounds hoping to live and fight another day.

Thus, a modest amount of selling can have an outsized impact on asset prices like we saw in December 2018. The result is when liquidity remains low, volatility increases. We must learn and deal with the reality that financial markets are run by machines and are highly automated.

The problem that arises when markets are this technologically complex and interconnected is you can get an unforeseen event that crashes the financial system similar to what almost happened with the collapse of Lehman Brothers and AIG in 2008.

Three Main Risks We See Hovering Over the Markets

The first is a policy mistake by the Fed. The markets reacted favorably to the recent dovish tone of the Fed. At a recent economic forum the Fed Chairman emphasized patience, looking more at weakening economic data and hinted they could throttle back on quantitative tightening.

On the dovish side of things, three of the new four voting members on the FOMC signaled they are willing to take more time to gain clarity about the outlook before doing anything with monetary policy. The most dovish, St. Louis Fed Governor James Bullard, warned the Fed risks pushing the economy into a recession if it raises rates further.

The recent comments by Powell and other governors lowered the probabilities in the futures markets to 75 percent that the Fed either holds rates steady this year or ends up cutting them. As of this writing, the Fed futures market predicts no rate hike until possibly June when probabilities rise to 21 percent, gradually increasing to 23 percent by September before falling back down to 21 percent by December. That’s the story now but it could change by summer if my thesis of rising oil prices plays out in the second half of the year. For now, the Fed remains on hold which is market positive. If history repeats itself, they will eventually raise rates high enough until they break something either in the markets or the economy and most times both.

The second risk is a trade war with China. Here too, there is hope it will be resolved. Recent reports show China’s economic expansion languished to its slowest pace in nearly three decades in 2018. The economic slowdown deepened in the fourth quarter decreasing to a 6.4 percent growth rate. President Xi Jinping initiated a stimulus program with economic growth as a top priority for 2019. The central bank added funds to the banking system to stimulate lending with possible tax cuts for business. However, the best move would be a far-reaching trade deal with the United States. China has resumed buying U.S. soybeans and withdrawn its retaliatory tariffs on U.S. cars signaling it wants a trade deal. Recent Trump tweets have been positive on getting a deal done.

I believe the trade war story will be resolved with both parties feeling they got something. Such a resolution will have implications for oil if China resumes its purchases. The lack of buying during negotiations was a contributing factor to U.S. inventory build.

The trade war is starting to impact American companies with rising material costs and shrinking sales. Think of Apple's lowering of fourth quarter guidance on revenues igniting a steep selloff in stocks last month. Given that we’re entering a presidential election cycle, I expect the trade war to get resolved, which will be market positive.

The final wild card, political discord, is playing out negatively right from the start. As of this writing, we are now 34 days into the government shutdown. Each week the shutdown remains in place it shaves off 0.10 percent off GDP growth for the quarter, costing $2.5 billion for every week the shutdown remains in place. The government’s fiscal budget this year is $4.41 trillion and we are shutting down the government over a wall and $5 billion dollars. That’s like arguing over a choice seat in a 50,000 seat football stadium.

It looks like political tensions and discord are in store for 2019 ad 2020 as we gear up for a presidential election cycle, leaving little hope for cooperation. There are proposals to raise marginal income tax rates back up to 70 percent, corporate tax rates back up to 28-30 percent, a $1 trillion dollar carbon tax, new proposed regulations, investigations and more talks of impeaching the president. So I don’t think compromise, peace and harmony are in the cards this year in Washington, which could create new uncertainties for the markets.

Given These Risks Where Does This Leave Us?

If the risks I have identified are resolved and Washington moves toward compromise it could be quite a good year for markets with positive returns for investors. If they aren’t resolved, we’ll see a repeat of last year where events will negatively dictate the outcome. This could lead to violent upswings or downswings depending on the news cycle, with movements exaggerated on the up and downside due to machine-driven markets and shrinking liquidity.

So what else could possibly go wrong? There are no apparent bubbles outside the one we have identified in passive index funds, which could exasperate any downside selling on any news-triggered event. Unlike 2000, technology stocks have largely corrected, especially the FAANG stocks. Real estate is weakening but not in a bubble. This leaves two possible financial shocks that could trigger a recession: an emerging market blowup or a meltdown in the U.S. corporate bond sector. An emerging market crisis could be averted if the Fed goes on pause, the dollar weakens and the trade war ends with China.

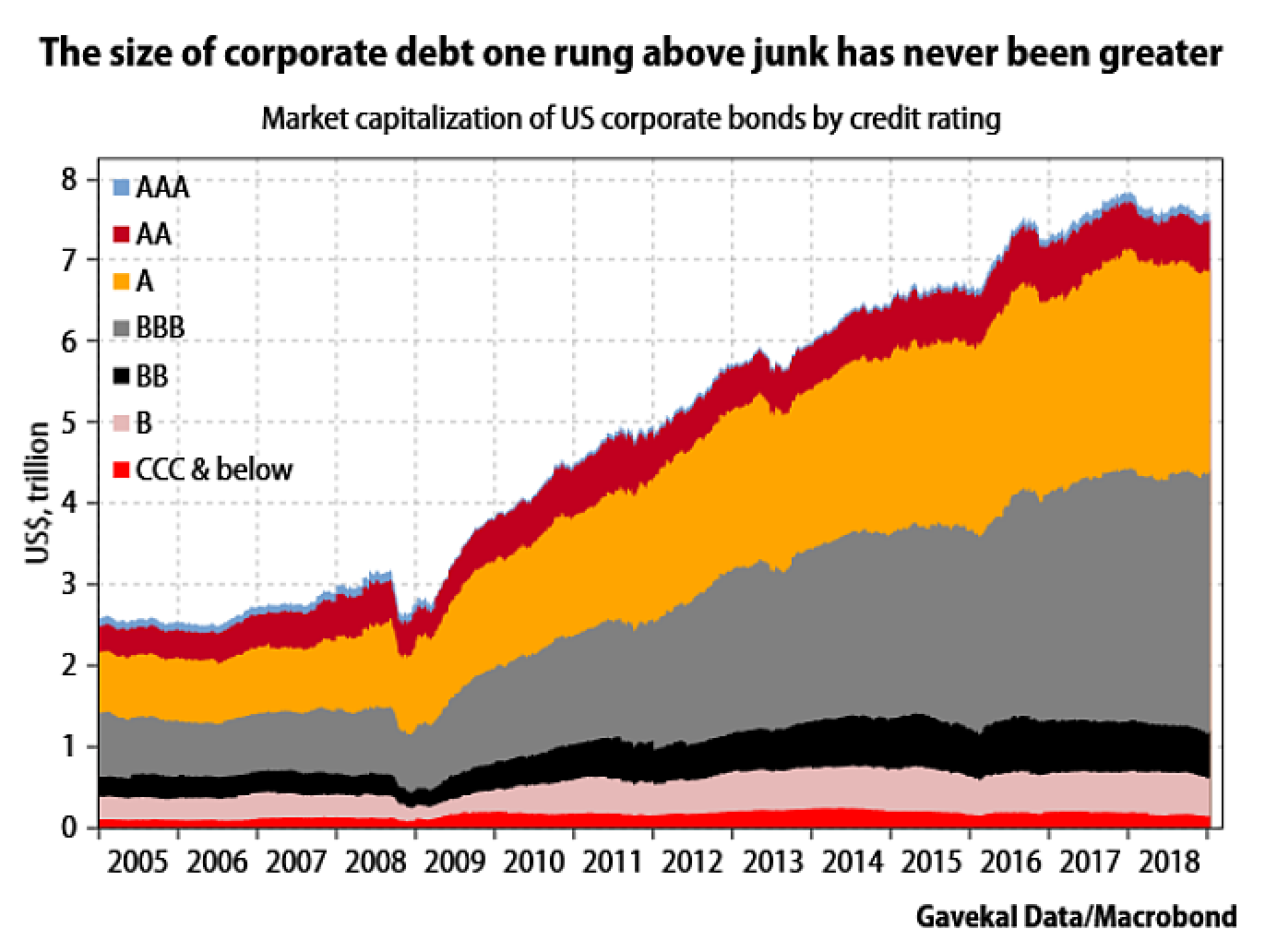

One risk we see as a potential financial shock lies within the U.S. corporate bond sector. Corporate debt is up nearly 60 percent in this expansion and a good amount of that debt is “BBB” rated. If you look at the entire corporate debt market, one-third is junk, one-third is BBB, and one-third is investment grade. The real crisis begins when the economy weakens or heads into a recession. A lot of those BBB-rated bonds will be downgraded forcing bond funds and ETFs to sell. This could be a crisis-driven event since the BBB market has exploded from $750 billion in 2007 to $2.7 trillion today as investors and institutions searched for yield.

What makes this scenario stand on edge is the composition of the bond market has changed during this recovery. In the past, high yield or low-quality bonds were the province of institutional investors, pension funds and insurance companies. In the last decade, as the Fed kept interest rates at zero after the Great Recession and bear market, retail investors piled into bond funds and bond ETFs in search of yield. There are a lot of bond funds and bond ETFs that sit on low quality and, importantly, illiquid bonds. These are bonds that bond funds or ETFs could not liquidate within a seven day period.

In the bond selloff last month, Bloomberg noted that a lot of these funds were forced to sell their high quality, liquid bonds in order to meet investor liquidations. This leaves them sitting on their low quality, less liquid bonds. If we get another downdraft in bonds or if credit spreads widen as they are doing now, this could bring about sudden losses and more liquidations.

Shrinking liquidity could also magnify any downward thrust in selling as a result of regulations. After Dodd Frank and other regulations were put in place, the major banks have reduced their bond inventories and their role as providers of liquidity. If you look at where we were a decade ago, bond ETFs totaled $15-20 billion and dealer inventories were in the $260-300 billion range. There was plenty of liquidity in the bond market. The picture has reversed today with inventories sitting between $30-40 billion against bond ETFs of $300 billion. In the event of a severe market selloff, liquidity has diminished as bond dealers’ ability to provide it has fallen by close to 80 percent.

In our opinion, the epicenter of the next financial crisis lies within our corporate bond market. In the words of Warren Buffett, “You don’t know who is swimming naked until the tide goes out.” Could it be GE which has $115 billion outstanding debt rated BBB? GE bonds are almost equal to 10 percent of the junk bond market. What occurs if they get a debt downgrade and what happens to all that debt owned by bond funds and ETFs that will have to be sold?

The Financial Times did a recent piece featuring Steve Eisman who shot to fame after Michael Lewis’s book “The Big Short” and subsequent movie. Eisman sees corporate bonds as another menace hovering over the financial markets. He is referring to the massive amount of bonds that have been issued in the BBB space, one step above junk bond ratings. He references a point I made back in 2017 about the shrinkage in dealer trading inventories as banks attempted to comply with new rules on capital and liquidity.

From our perspective, the likely epicenter of the next crisis is not the banking sector. The crisis is likely to surface in the corporate bond arena which will accelerate as a result of shrinking liquidity. This could force painful, steep discounts and big market losses on the funds who hold these bonds.

Wall Street is currently bullish on the markets and the economy similar to where they were last year. The bullish forecasts are predicated on the economy continuing to grow, corporate earnings up in the 7-8 percent range, and a recovery from an oversold condition at the end of last year. Few are talking about the potential of a recession next year if the Fed continues to tighten. If there is a recession coming it certainly isn’t reflected in any forecast we have seen with consensus economic growth at 2.6 percent for this year and 1.9 percent next year. An economic growth rate of 1.9 percent doesn’t reflect a recession but is more in line with economic growth over the last decade. The bears are few in number. I could only find one economist out there, our friend A. Gary Shilling, who has a two-thirds probability of a recession hitting this year.

Our own view is one of caution as 2019 will be event driven, unpredictable and volatile. Therefore, we remain defensively positioned, letting events and the markets determine the outcome and where we need to be invested. For the moment, what we don’t know is how these events will unfold. What we do know is volatility is back and likely to stay.