Step over here for a second while I walk you through some macro events that are likely to shape markets over the next few months. The taper trade has been taking shape over the last month since the decent employment data for April and the Jon Hilsenrath article, “Fed Maps Exit from Stimulus”, have reintroduced the exit plan for the Federal Reserve’s purchases of bonds. Since the Fed will stop buying as many Treasuries or mortgage-backed securities, mortgage rates and Treasuries yields have risen this month. Additionally, equities have moved higher based on better economic numbers, but also lower on taper talk from Federal Reserve Presidents as well as from the FOMC minutes last week. It seems that there is some debate in the market whether tapering is good or bad. One thing is for certain, rates have risen and that may be causing another wave of asset and stock rotation in the market.

A couple of weeks ago, I wrote about the Taper Trade, which is pro stocks (cyclical stocks especially), stronger economic growth, and less Fed accommodation. Less Fed accommodation means less support for U.S. Treasuries weaken (yields rise), dollar strengthens, and commodities weaken. I should have been more forthright about commodities weakening. Economically sensitive commodities will do well if the economy does well. That’s why copper has been holding up well in May. Precious metals, which are more sensitive to monetary policy, would weaken if the Fed is less accommodative. We’ve seen gold and silver retest the April lows this month based on the taper discussion; however, if the economy can continue to strengthen (as well as global growth), and rates move up based on that economic strength, then all commodities will rise in a reflationary trade. Higher factory utilization rates and a growing global economy can reverse the negative trend in commodities that began in April of 2011 when China’s stock market topped.

I continue to focus on the fact that cyclicals continue to outperform non-cyclicals. That wasn’t any more evident than on Tuesday. Tuesday, Treasuries plummeted and yields rose on a record trading day in Treasury futures. 10,476,906 futures contracts traded hands, surpassing the previous record on February 26th of this year according to the CME Group. TLT was down nearly 2.5% and bond-proxies in high yielding defensive stocks came for sale while financials were mostly positive on the day.

Cyclical stocks continue to be the strong area of the market. There is a rotation taking place as I mentioned a couple of weeks ago. Despite the consolidation in stocks since last Wednesday, it’s encouraging to see that this trend hasn’t changed. Normally, if we were going to be looking at a month to two-month consolidation or narrow correction in stocks, we’d begin seeing the risk off trade and defensive areas in stocks outperform – but that’s not the case.

Financials continue to be my favorite area in the market. That’s because a steepening yield curve helps net interest margin, something analysts have been complaining about over financials for the last few earnings seasons. Heck, it seems like banks cannot fail. Bank stocks go up if rates drop because more mortgages will be refinanced. If the yield curve widens as long-term rates go up, they make more interest income on the spread of loans and deposits. Big money centers are hitting fresh 52-week highs and securities broker/dealers are making a comeback as investors attracted to performance in stocks return from their cash hiatus. Insurance companies continue to perform well as well. When all of the subgroups of a major industry are working, that’s an incredibly good sign.

Other cyclical areas that are outperforming are energy, materials, industrials, and tech. Now if you only look at the tech sector through the incredibly Apple-dominated ETFs, then you’re going to get an incredibly deceptive idea of what’s really going on in the rest of the sector. For instance, many semiconductors produced ok 1Q results; however, but many have an improving outlook for the next quarter citing double-digit growth in mobile/wireless like for Marvell Technology Group (MRVL). Analog Devices (ADI) recently announced a 60% cash flow payout increase to 80% in dividends and buybacks. JP Morgan had its 41st Annual Technology Conference just a couple of weeks ago with companies including Texas Instruments (TI), Advanced Micro Devices (AMD), Maxim Integrated (MXIM), and Microchip Technology (MCHP). They said that coming away from the conference, almost every semiconductor company stated order rates and backlog continue to grow. From a technical standpoint, some of these companies couldn’t look more attractive on the charts, having been beaten up on PC sales figures over the past few quarters. Fundamentals and technical charts are matching up for the group. Note the relative performance (to the S&P 500) in semiconductors versus the Apple-heavy tech sector ETF. Even Apple’s chart is beginning to look more constructive.

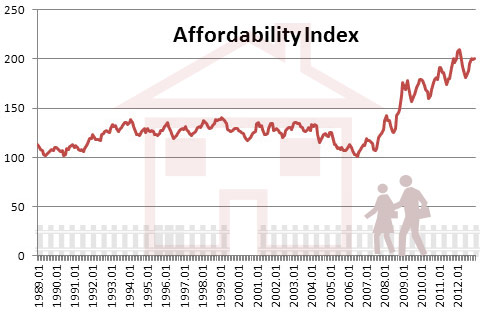

Right now, some investors are concerned about housing and the economy if rates climb. I’m not. The article I wrote in March, “Housing: This Bull has Room to Roam”, explains that the affordability index is still at record high levels due to fallen housing prices and interest rates. There will come a time when rates will be much higher and eventually, the screaming demand we’re seeing from both investors and homeowners will apex, but that isn’t here at at a 30-year mortgage rate of 3.94% - near multi-decade lows. The National Association of Realtors’ Affordability Index has dipped recently as mortgage rates have crept up, but it is still near record levels near 191 in March (it bottomed at the housing peak at 100). It may have peaked at 210 in January, but that doesn’t mean the recovery is over. Normally, this indicator has been hovering around 130 for most of the 1990s. Call it a mini-bubble if you like. The attractiveness of profits for private investors buying houses at low price and low rates is alluring and will not be here much longer; however, I don’t think that the removal of these buyers will stop housing prices from recovering. Housing prices will keep on rising as long as there is money supply and loan growth as well as economic growth,

1-Year Affordability Index

Data Source: NAR

Historical Affordability Index

Data Source: NAR

Concerning gold, the near-term is improving and attempting to form a double-bottom. The intermediate trend will significantly improve if gold can close above $1415. If it can do that, technically speaking, it will likely re-test $1450 to $1475 (where the significant 50-day moving average is currently). If gold can get above its 50-day moving average, then we can start talking about double-bottoms. Failure to break $1415 would likely turn into another test of the lows. Gold and silver were severely oversold in April, which led to an oversold rally. There is still no sign of confirmation that gold and silver have broken their long-term declining trends. Eventually, we believe there will be a reflation trade again in gold, but it’s hard to tell if that’s now or later. We believe that gold is merely moving higher on the recent taper talk that is suggesting nobody look for a policy change until September at the earliest since the recent FOMC minutes, despite Fed hawks that want a taper as of yesterday. Gold will likely be in a trading range or worse until the Fed acts on its taper talk.

Long-term rates have been a focus of market strategists over the past two years. Many expected rates should be much higher based on Fed intervention. The European Sovereign Bond crisis proved them wrong as a flight of capital found refuge in U.S. Treasuries and the dollar. With equities indices hitting new all-time highs, sentiment is beginning to change, but not completely. This is still the most unloved bull market I’ve seen, and that means the S&P multiple can move higher. The recent shift out of non-cyclical stocks into cyclical stocks bodes well for equities and suggests that corrections will continue to be shallow, thanks to the Bernanke put and a global shift away from austerity that started with President Hollande’s election in 2012. Especially as European and Asian politicians grow increasingly concerned over the jobless rate of the young.