Two days ago, OPEC warned the world could be facing the worst-ever oil supply shock and that it will be 'nearly impossible' to replace Russian oil. In the following article reprinted from May 2020, Financial Sense's Jim Puplava explained the difficulty OPEC nations face in producing more oil and why investors should position for a coming energy shock and much higher inflation. Note: when this article was first published in 2020, West Texas oil was trading around $20-30 per barrel and official inflation was 0.1%. As of today, West Texas oil is trading at $104 per barrel and headline inflation is now growing at 8.5% yoy. For our most recent audio commentary and outlook, see $150 Oil, the Next Energy Crisis and a Decade of Higher Inflation.

“If you look at the top 20 companies of the world, 19 of them are still brick and mortar companies. What I am saying is that if you have a car manufacturer or an oil and gas manufacturer, you won’t get supply over the Net.”

–Anil Ambani

“Always expect the unexpected. The oil and gas industry is terrible at predicting anything. Always have a back-up plan.”

–David Dixon

The Perfect Energy Storm

It came out of nowhere. No one saw it coming. A perfect energy storm. A global pandemic. A price war between two of the world’s largest producers, and a supply surge from US shale production, all converging together to create the greatest unforeseen demand destruction. The oil market went through one of the worst months in its entire history, with demand plummeting by 20 to 25 million barrels per day (mbd). The destruction of demand couldn’t have come at a worse time as a price war between Saudi Arabia and Russia moved vast amounts of oil onto the markets while record US shale production added to the supply glut.

Prices plunged to levels never seen before. A 300% drop in a single day with futures markets well into negative territory as a large seller scrambled to find buyers for its unwanted contracts at a time of limited storage. Cushing was at 85% capacity while Reuters reported 160 million barrels of crude held in floating storage on the ocean via crude oil tankers. Currently, there is so much oil sloshing around the globe that sellers are looking everywhere to store the stuff, from tankers anchored at sea, river barges, large cylinders, to salt caverns. The President even talked about opening up the Strategic Oil Reserve for excess inventories. We are simply running out of places to store these unwanted barrels.

Oil demand dropped from a record peak of 100 mbd reached in 2019 to a recent low of 70 mbd. Decades of demand growth were wiped out quickly in a single month. Nothing in the history of oil can compare to the events we have witnessed in the last three months as planes stopped flying, cars remained parked in garages, and factories and stores closed around the world as country after country went into lockdown mode.

Now, the media is filled with reports that we have reached peak demand with projections that energy demand will remain anemic for years to come. Negative growth in demand is forecasted to continue as we transition to clean energy.

The problem with these reports is that they are linear in scope, projecting current events well into the future, often based on model projections that are backward-looking. Just as so many of the COVID-19 projections were off by a factor of ten, so will these demand destruction and supply projections prove to be off base. Instead of a perpetual supply glut and falling demand, we are more likely to be facing an oil shock as oil supply is about to collapse.

Stay ahead of the news! Subscribe to our premium weekday podcast

At $20 oil, no one is making money and if prices continue at these levels for the next year, just about every oil company will be on life support or out of business, including half of OPEC bankrupt. Even OPEC behemoth Saudi Arabia is at risk of financial collapse. During the last price war in 2014-2016, Saudi economic minister Mohammed Al Tuwaijri stated that without reform measures, and if the economy remained the same, they were doomed to bankruptcy in 3-4 years. This was made in reference to the kingdom’s efforts to overproduce and push down oil prices just as it did this year. And that comment was made at a time when Saudi Arabia’s foreign exchange reserves were over $730 billion. Today, those reserves are at $464 billion, the lowest level since 2011. To deal with this crisis, Saudi Arabia has imposed austerity measures from an increase in its VAT tax to eliminating allowances for state workers in an effort to bolster battered state finances. Once again, the recent price war has backfired and jeopardized the kingdom’s finances. More about Saudi Arabia later.

Fall in Shale Production

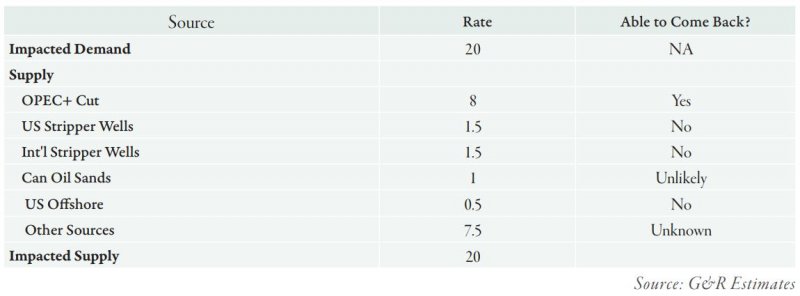

Lets now consider the future oil supply dynamics. Looking at supply, it is ready to fall off a cliff. Factor in the OPEC+ production cut of around 9.8 mbd, production cuts from Norway, and a steep fall-off in US shale production, and offshore supply could drop off by an amount equal to the drop in demand. As shown in the table below, the fall-off in supply will take years to come back since once a well is shut-in it may become uneconomic to bring it back online.

The US oil rig count over just the last six weeks is down over 45% and continues to decline as every shale producer, including major oil companies, cut back on drilling. Exxon (400K), Chevron (200k), and ConocoPhillips (260K) alone are cutting back production by hundreds of thousands of barrels a day. Continental Resources has curtailed 70% of its operated oil production in May. Experts believe the 2020 US oil rig count could be down by nearly 75% from 2019 levels.

$20 Oil Unsustainable

Simply put, $20 oil doesn’t work for anyone, including OPEC. Most need $46 a barrel on average in the Permian and Eagle Ford to drill new wells and $51 on average in the Bakken. Many OPEC countries need higher oil prices to balance their budgets, including $70-$80 a barrel for Saudi Arabia.

What is not clearly understood is that once oil inventories reach maximum capacity, the oil markets will immediately become balanced. For once storage facilities are full to the brim, the entire global petroleum industry will be forced into shutting down and switching to a just-in-time supply chain dynamic. You don’t produce oil when there is no place to ship or store the barrels you produce. Excess production will drop off rapidly as wells are shut-in. As shown in the tables above from Goehring & Rosencwajg, many of those supply reductions will occur in stripper wells both here in the US and globally. These are wells that produce less than 5 barrels per day and make up nearly 20% of US aggregate production. Those stripper wells are marginally economic and would never justify the capital costs to drill and bring them back online when they only produce 5-10 barrels a day.

According to Rystad Energy, US production could be down by 2 mbd by the end of June and maybe more if storage runs out and wells begin being shut-in. Many wells will never come back online resulting in lost production. Shutting in a well for a prolonged period of time can damage the wellbore or reservoir. In addition to low producing stripper wells, US shale was already showing signs of peaking during 2019 when the rate of production growth and well productivity was already in decline.

Most Oil Comes from Giants 75 Years Ago

Factor in that much of our oil comes from just 25 oil fields discovered over 75 years ago with most of them already in decline, and future supply becomes even more uncertain. The worlds’ 507 giant oil fields (those that produce more than 500 mbd) make up about 1% of all oil fields, but they produce 60% of the current oil supply. The majority of these fields are over 50 years old, with the largest Ghawar (Saudi Arabia, discovered in 1951), Burgan (Kuwait, 1945), Safaniya (Saudi Arabia, 1957), Rumaila (Iraq, 1955), Bolivar (Venezuela, 1917), Samotlor (Russia, 1964), Kirkuk (Iraq, 1934), Berri (Saudi Arabia, 1964), Manifa (Saudi Arabia, 1964), and Shaybah (Saudi Arabia, 1998).

The study of these oilfields was documented in Frederik Robelius’ book, “Giant Oil Fields – The Highway to Oil.” Its key takeaway being that once these oil fields peak, enhanced recovery techniques may postpone their decline but at the added expense of a more rapid decline later. Most of these fields are already experiencing 6-7% decline rates and we are simply not discovering “giants” anymore. Simply said, it will become progressively more difficult for new discoveries to replace declining production from existing giants.

Even trying to replace these declining fields will take trillions of dollars of new investment, which is not happening. Investment peaked in 2015 at $1079 billion, falling to $583 billion by 2016. With the plunge in oil prices, hundreds of billions of needed investment has been canceled or postponed. Instead, since 2016, the mantra on Wall Street for energy companies was to slash expenditures, buy back stock, and increase dividends. With the exception of companies like ExxonMobil, few companies were investing in upstream operations.

Even if investment began today, it will take time and money to find and then bring production online. Given the damage done by shut-ins, many of these wells will not be coming back online. The industry has never witnessed anything like what it has experienced over these last few months. It may seem farfetched right now but given these dynamics, one can imagine that a new oil price cycle has begun leading toward another future oil shock.

Saudi Arabia's Reserves Overstated

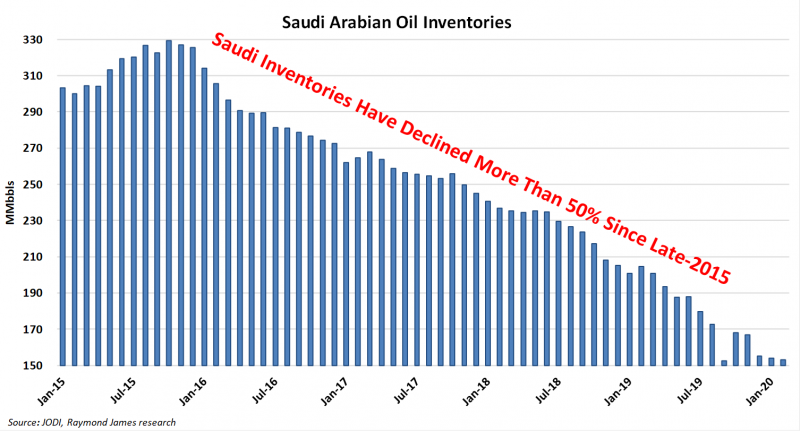

Before moving on to demand I want to address one final supply issue: Saudi Arabia. The world has been operating under the long-held assumption that the kingdom was the supplier of last resort. It is widely believed the Saudi’s could produce 12.5 million barrels a day leaving it with a spare capacity of 2.5 mbd. The truth of the matter is they have never produced at that rate. Those extra 2 million barrels came out of Saudi inventory, not production.

The other issue is the kingdom’s “actual” oil reserves, currently estimated to be 266 billion barrels. In 1989, they were miraculously increased from 170 billion barrels to 266 billion, despite daily production of 9-10 mbd. How could their oil reserves have remained unchanged for nearly 30 years despite their annual production of close to 3 billion barrels of oil every year? The Saudi response is that they simply replace what they produce with new discoveries. Why are their unchanging reserves, production capabilities, and spare capacity simply accepted despite the fact that their largest oil fields, Ghwar (1951), Safaniya (1957), Manifa (1964), and Berri (1964) were discovered more than 50-70 years ago and are now in decline? Experts in the field believe the kingdoms’ true spare capacity is closer to 0.5 mbd than the widely claimed 2.5 mbd.

When it comes to oil there are really only 5 key players: Saudi Arabia, Russia, US, Iran, and Iraq. Of the five, only two—Iran and Iraq—have the greatest potential to increase production and the greatest potential for new discoveries.

The Next Black Swan

As to demand, the picture too is rather uncertain. Oil experts hope the bottom for oil has been reached as economies start to open and move gradually out of lockdown mode to resume normal functioning, whatever that may look like in the future. No one knows what normal will be when we completely reopen again. But there are encouraging signs both here and abroad that demand is starting to pick up again. Demand in China is growing and refinery runs here in the US have increased from 12.8 mbd to 13.2 mbd as of April 24th.

From China to Europe to the US, people are gradually returning to driving their cars as countries reopen for business. As a result of social distancing, people feel safer commuting in their own cars than they do using public transportation. We are seeing an increase in commuter driving and increased expectations for road trips instead of flying for vacations this summer. Major oil firms with retail fuel operations are reporting the use of cars is now the preferred way to travel.

As economies reopen, people will likely use public transportation less, given that subways, buses, and trains have been a major, if not primary, transmission of the virus. Airlines may suffer in the short-run mainly due to business travel being replaced by online conferences, but the main method of transporting people and goods will still remain fossil fuels. We may be transitioning to a greener economy, but the primary form of transport will remain the combustion engine for cars, trucks, tractors, and planes.

In summary, there is a saying in the oil industry that “the cure for low oil prices is low prices.” As prices have fallen and remained low over the last six years, needed investment has been curtailed, projects shuttered, capex slashed as more investment has been needed to replace depleting oil wells old and new. Depletion is relentless, it is increasing, and it knows no price. It is geological and is taking place daily. Barrels produced are not being replaced. As storage levels top out, the markets will be balanced, and a major shut-in will take over, reducing production to equal demand. The problem is much of that demand will not come back as it can’t be turned on and off like a light switch. Few see this or acknowledge it, but the next black swan is likely to be an oil shock or a major geopolitical event in the Middle East.

An Uneasy Transition

Finally, it is important to discuss the transition to clean or “green energy”. There have been numerous articles recently about peak demand. I have addressed this issue before on my weekly podcasts stating my belief that this transition may not go smoothly, take longer than expected, and will not work for many countries.

As Peter Zeihan discussed in his latest book, "Disunited Nations: The Scramble for Power in an Ungoverned World," energy is the lifeblood of our industrial way of life. Without energy there is no industrial lifestyle; everything from cars to cabbages to cell phones to condoms requires the petroleum economy. Europe imports some 90% of its oil and natural gas from, in decreasing importance Russia, the Persian Gulf, and North Africa. East Asia imports a similar proportion of its needs, upwards of three-quarters of it coming from the Persian Gulf. For the most part, the oil is not where the people are, and it is only the current international order (i.e. American military might) that has enabled the oil to reach the people with minimum fuss.

The Geological Survey of Finland confirmed Zeihan's thesis in their recent survey, “Oil from a Critical Raw Material Perspective.” Oil remains and will remain, the backbone for approximately 90% of the supply chain of all industrial manufactured products which depend on the availability of oil-derived products, or oil-derived services. Energy is the master resource. It allows and facilitates all physical work done, the development of technology, and allows human population to live in such high-density settlements like modern cities. In 2018, the global system was still 84.7% dependent on fossil fuels, where renewables accounted for 4.05% of global energy generation.

As Zeihan and the Finland survey contend, energy, especially fossil fuels, will remain a critical resource for our industrial/technological society for decades to come. We are in a period of transition to a new greener economy that will take decades to transform. In the meantime, oil will remain a critical necessity. As economies recover, so will demand for energy. This time however, it may not be readily available at current prices due to supply destruction as a result of “The Perfect Energy Storm.”

Unloved, Undervalued, Underowned

This leads me to consider energy as an investment, which has certainly been out of favor with Wall Street. See the graph below comparing the energy ETF, XLE, and the performance of the S&P 500 over the last decade.

I believe this out of favor, underperforming sector is about to change in the 2nd half of this year and going into 2021 when I expect oil prices to surge absent another pandemic outbreak.

Another chart that favors oil is the gold-oil ratio. Because of the COVID-19 pandemic, the ratio has reached the highest level in history as shown in the graph below. This indicator has been a reliable tool as to when to invest in either commodity over the last century.

Presently (as of 5/18/2020), an ounce of gold ($1,732) will purchase 52.9 barrels of oil ($32.74). Historically, the gold/oil ratio has spent most of its time ranging between 10-30 over the last 100 years. Viewing this ratio over time, it swings from one extreme to another which relates to the supply of the commodity. Clearly, this ratio is now flashing a buy signal.

The Return of Inflation

There are other reasons that argue for both oil and gold. In addition to an oil shock, the other black swan no one is expecting is the return of inflation. As stated in my article, “The End of Money,” when you have economic and market shocks, the first wave is deflationary as asset prices fall and economic activity contracts. That is what we are experiencing now. The article also addresses the massive amounts of both fiscal stimulus and monetary stimulus yet to come in the years ahead. The production of goods has been curtailed with the lockdown and will possibly remain as many Democratic governors keep their states shutdown, including industrial states such as Michigan, New York, California, and Pennsylvania. At the same time that production and services are being curtailed, trillions of dollars of newly created money is being distributed to individuals and companies to spend in order to keep the economy from collapsing.

As shown below, the Fed’s balance sheet has gone from as little as $800 billion in 2007 to its current value of over $6 trillion, growing at nearly $1 trillion a month. The Fed is backstopping every asset in the financial system from Treasuries, mortgages, commercial paper, money markets to now corporate bonds and ETFs. Congress has already proposed another $3 trillion stimulus bill which is in the negotiating phase and the President is working on a $2 trillion infrastructure bill. Modern Monetary Theory (MMT) is providing the intellectual framework for spend and print. In the last monetary up-cycle, money remained at the Fed or went into financial assets. This cycle, it is more likely to end up in inflating goods and services as the Fed is pushing money into risk assets.

So where does all this leave us? The media and the financial markets are clearly pushing the deflation narrative and the end of energy and peak demand. I don’t buy these arguments and neither should you as a study of history would argue otherwise.

When it comes to using the media as a contrary indicator, I am reminded of certain magazine covers in thinking about the theory of opposites and the art of contrary thinking. On August 13, 1979, Businessweek (now Bloomberg Businessweek) heralded “The Death of Equities” just two years before one of the longest-running bull markets in stock market history. More recently, the April 20, 2019 cover of Businessweek asked "Is Inflation Dead?"

I leave it up to you to decide but as for me, I am betting on oil and inflation.

“Control oil and you control nations; control food and you control the people.”

Henry Kissinger

“The best business in the world is a well run oil company. The second best business in the world is a badly run oil company.”

“I’ve always tried to turn every disaster into an opportunity.”

“The way to make money is to buy when blood is running in the streets.”

John D. Rockefeller

To find out more about Financial Sense® Wealth Management or for a complimentary risk assessment of your portfolio, click here to contact us.

Advisory services offered through Financial Sense® Advisors, Inc., a registered investment adviser. Securities offered through Financial Sense® Securities, Inc., Member FINRA/SIPC. DBA Financial Sense® Wealth Management.

Copyright © 2022 Jim Puplava